We have heard, “Blockchain Technology,” being used a lot ever since late 2010s. We instantly associate it with Bitcoin, but it’s not exactly the same. In this article, I will explain, in a layman terms, what on earth is a blockchain technology, and why is it so popular. So, let’s go:

What is Blockchain Technology

What is it: At its core, blockchain serves as a fixed ledger, resistant to alteration, hacking, or manipulation. When I say ledger, simply imagine a place full of transactions, like spreadsheet, (Bob sent 5$ to Stacy, Mya sent 10$ to Steve, and so on.) This ledger is decentralized, meaning, it’s distributed across huge network of interconnected computers (They are also called nodes). Essentially, there is no one centralized place or server where this, “blockchain,” is operated on; rather, it’s operated on a network of computers, each containing exact copy of the blockchain transactions. There is no single point, rather multiple points. You can probably already tell why that is a very good idea, and how safe it is compared to anything else.

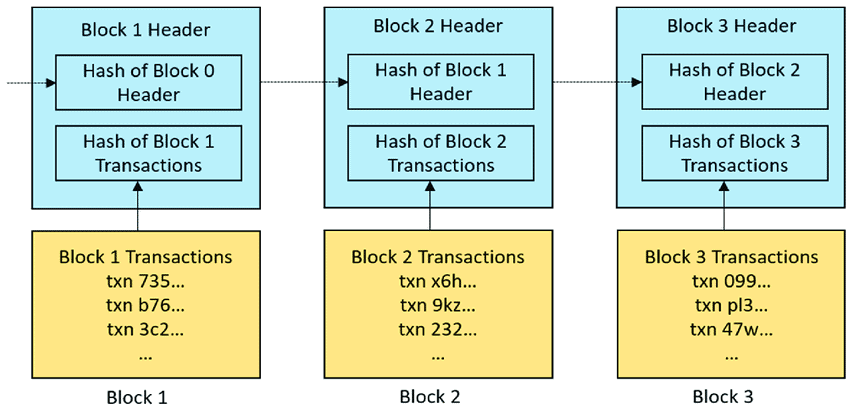

Chain in blockchain: Basically, blockchain functions as a digital ledger, containing transactional records, also referred as blocks. After certain time period, there’s a new block created, hence the “chain,” in “blockchain.” So, basically, it’s a chain of blocks, each block containing information of recent transactions, and this chain goes all the way back to very first block/transaction. This network operates through peer-to-peer nodes, the computer network that I mentioned, ensuring decentralized control and transparency. So, no one computer or entity really controls the said blocks.

Block: As I mentioned, one should imagine this digital ledger as a shared spreadsheet among network of computers. Here, transactional records are stored, reflecting real-world purchases, with the crucial caveat that while data is visible to all, it remains incorruptible, meaning, no one can manually alter it, once transaction occurs, it will be there for eternity.

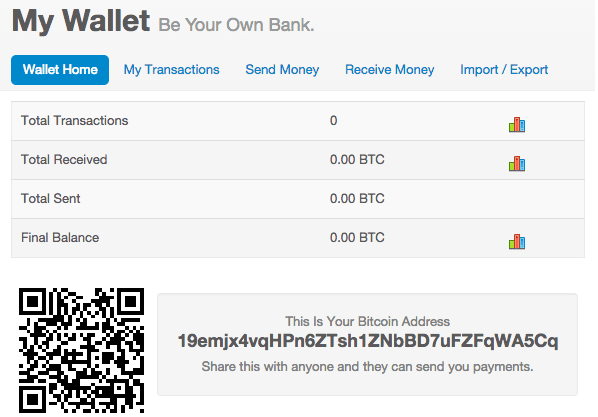

Transactions: For transaction to occur, you need your own wallet address within the blockchain network. Don’t worry, this address doesn’t show your IP, it’s simply string of random numbers and letters (See the image below). Each transaction within the blockchain is authenticated through the digital signature of the owner, guaranteeing its integrity and security. You don’t have to actually sign anything, it’s done automatically. So, one can’t fake or duplicate the spending, even if you are tech savvy. This decentralized nature ensures that while data is accessible to all, it remains safeguarded against hacking.

Key Features of Blockchain Technology

So, to narrow down key features of a blockchain technology:

- Security: Blockchain employs digital signature mechanisms to facilitate fraud-free transactions, making data manipulation and transaction meddling impossible.

- Decentralization: Unlike conventional systems reliant on regulatory oversight, blockchain transactions are facilitated through the network of computers. No one can act as a third party overseer of transactions. It’s peer to peer. If there’s any major decision to be made, it’s made through mutual consensus among users. This decentralized architecture minimizes reliance on single points of failure and mitigates data manipulation risks.

- Automation: Blockchain’s programmable nature enables the automatic execution of actions, events, and payments upon meeting specified trigger criteria. So, again, you don’t need to be tech savvy to make transactions through blockchain technology.

Anatomy of Blocks

Blocks within a blockchain comprise of three integral components:

- Hash: A unique cryptographic value representing the entire block. Look at it as a tag, a label, of an individual block. Each block has its unique hash, which differentiates it from other blocks.

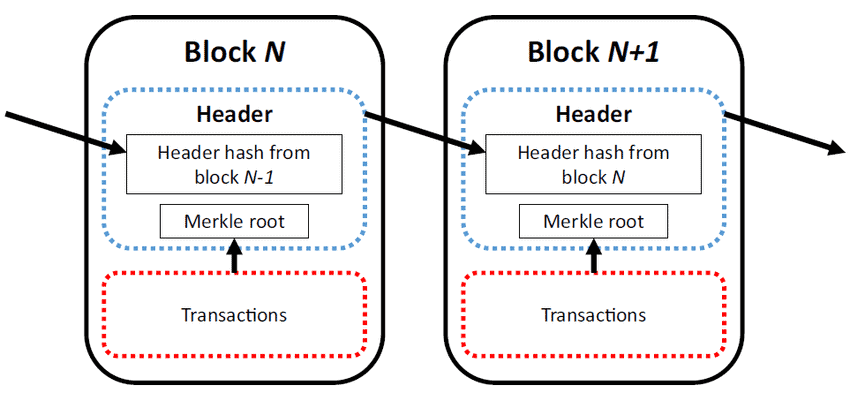

- Header: Contains metadata such as timestamps and previous block hashes. This ensures blocks are “chained,” and best way to do that is to have information of previous blocks in the header of a next block.

- Transaction Data: Houses main transactional information stored within the block. So, a spreadsheet body basically, that we talked about.

Block time is the duration required to generate a new block within the blockchain. Block time can be, and is, different across different blockchains. Shorter block time facilitates faster transaction confirmations, but increase conflict potential as there’s less time for confirmation.

Mechanism of Blockchain

Okay, let’s get little bit technical. It’s not hard to understand, trust me. Blockchain operates at the intersection of three core technologies:

- Cryptographic Keys: Consisting of private and public keys. As names suggest, private key is something only the person should know, while public key is how your wallet looks for, well, public. Both, public and private keys, are string of numbers and letters. Your wallet address is public key. Cryptographic keys serve as digital identity references.

- Peer-to-Peer Network: As mentioned many times, the decentralized computer network. It has many names, like distributed ledger, decentralized network, nodes, peer-to-peer network. Idea here is that all this transactions, and all this blocks, aren’t owned by one entity or server, it’s shared among the network of users.

- Computing Infrastructure: Serving as the backbone of the network, computing infrastructure stores transactional records and facilitates network operations. It’s a program basically.

Creating a block

There are many ways how blockchain technologies choose to create new blocks, two major ways are Proof of Work and Proof of Stake

Proof of Work

Proof of Work Puzzle: Across the globe, numerous individuals engage in a computational race to find a hash value that fulfills a predefined criterion. You may remember that each block has it’s own hash number. This endeavor is undertaken via computational algorithms, with participants striving to crack a mathematical puzzle known as “the proof of work problem.” Successful puzzle resolution creates a new block. In essence, blockchain miners endeavor to decode this puzzle, with the first successful solver reaping a reward in form of native cryptocurrency of a said blockchain technology. So, yes, there’s a financial incentive for mining.

Bitcoin vs Blockchain

So, what’s the difference between the two?

Bitcoin: Bitcoin is a cryptocurrency, that is used on Bitcoin Blockchain. So, Bitcoin is how you interact with Bitcoin’s Blockchain technology, it’s simply a currency, for miners to get as a reward, and for users to use it as a money.

Blockchain: Blockchain is the infrastructure on which Bitcoin is built on. All the things we talked about in this article from decentralization to hashed, to transactions, all occur here.

Of course, there’s way more to it, but for the sake of simplicity let’s finish here. All the fundamentals are above, Cryptosneed will be writing more articles on this topic to delve deeper, so stay tuned.

8 Comments

Comments are closed.